AI Robo-Advisors: Are They Better Than Human Brokers? Let’s Dig In.

Alright, let’s cut the BS. You’ve heard the buzz. AI’s everywhere, and now it’s coming for your money. Robo-advisors. They promise cheap, easy investing. But are they really better than a flesh-and-blood human broker? The honest answer? It depends. It’s not a simple yes or no. We’re talking about your hard-earned cash, after all. You want to make smart choices, not get blindsided by jargon or a machine that doesn’t understand your gut feelings. Let’s really look at the facts.

Source : vacuumlabs.com

The Rise of the Machines

Remember the old days? Stuffy offices, guys in suits whispering about stocks. That’s the classic image of a human broker. They had the inside track, or so it seemed. Now? We’ve got algorithms. These AI robo-advisors are essentially computer programs. They use fancy math and data to manage your investments. No coffee breaks, no bad moods, just pure data crunching. They’ve exploded onto the scene because, frankly, they’re cheap and accessible. You can often open an account with just a few hundred bucks. Try doing that with a traditional advisor.

What Exactly IS a Robo-Advisor?

Source : techtarget.com

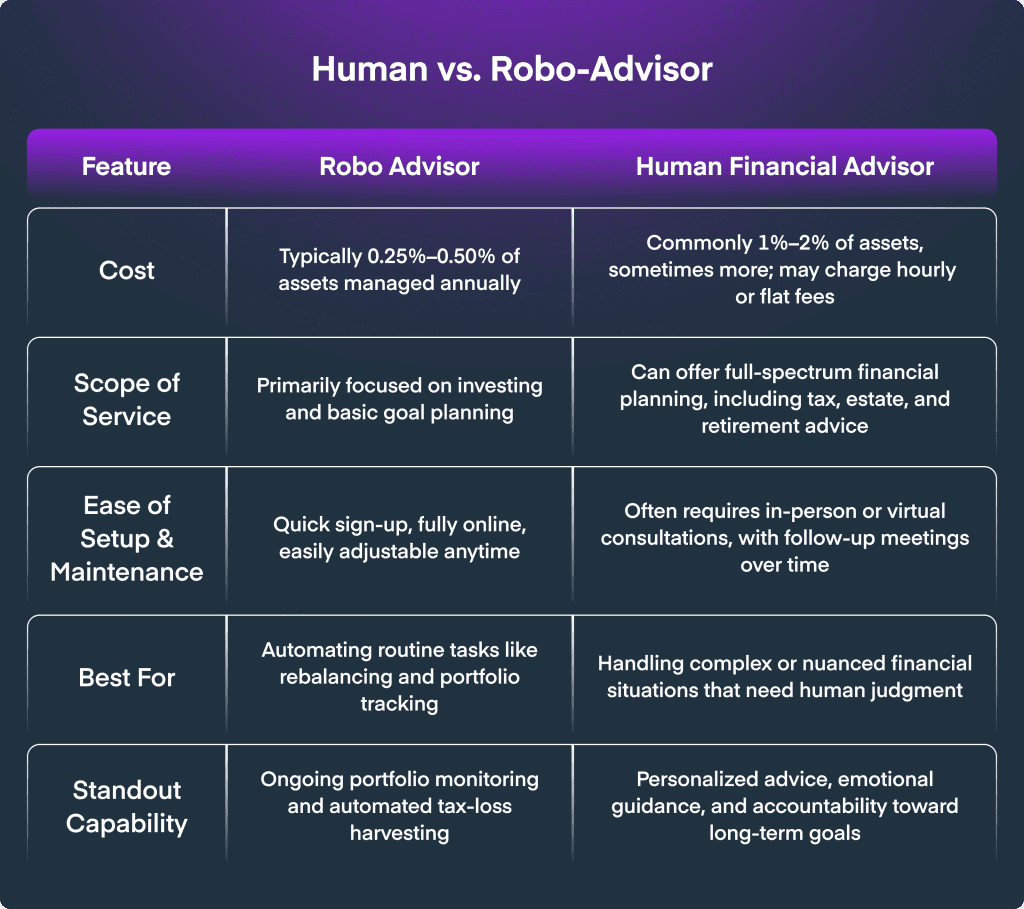

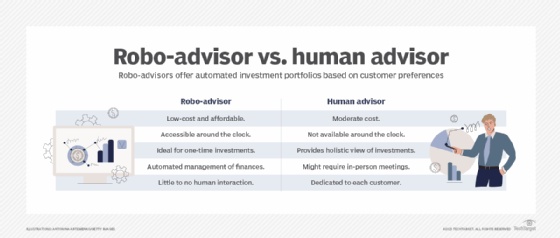

Think of it like this: you tell the robo-advisor your goals – retirement, buying a house, whatever. You plug in your age, how much risk you’re comfortable with, and how much dough you have. The software then spits out a suggested portfolio, usually a mix of low-cost Exchange Traded Funds (ETFs). It’s all about diversification and passive investing. They rebalance your portfolio automatically, too, so you don’t have to lift a finger. It’s pretty hands-off. Easy, right? For a lot of people, especially younger investors just starting out, this sounds like a dream come true.

Why People Love Robo-Advisors

Let’s be real, the biggest draw? Cost. Human advisors typically charge anywhere from 1% to 2% of your assets under management each year. If you have $100,000 invested, that’s a cool $1,000 to $2,000 every single year, gone. Robo-advisors? They usually charge 0.25% to 0.50%. That’s a massive difference over time. On $100k, you’re looking at $250 to $500 a year. Plus, you can often get started with a much smaller amount of money. Many have no minimums at all. It’s democratizing investing. You can also access them anytime, anywhere, 24/7. No scheduling appointments. Just log in and see your money. It’s incredibly convenient for busy folks.

The Human Touch: Why It Still Matters

But here’s the rub. Investing isn‘t just about numbers. It’s about emotions. Life happens. You might have a sudden job loss, a health crisis, or a complex inheritance situation. Can a robot truly understand the nuances of your panic, your hopes, your family dynamics? A good human advisor does more than just pick stocks. They’re coaches, therapists, and strategists all rolled into one. They can help you navigate market downturns without selling everything in a panic. They can explain complex financial products. They can help you plan for specific, unique life events. This kind of personalized guidance is something most robots can’t replicate. It’s about building a relationship, not just executing trades.

Source : msn.com

When a Robo-Advisor Might Be Your Best Bet

So, who are robo-advisors really for? If you’ve got a straightforward financial situation, you’re comfortable doing your own research, and you’re primarily focused on low-cost, diversified investing for long-term goals like retirement, a robo-advisor could be perfect. Think of someone who just needs a simple, automated way to invest their 401(k) rollover or their spare cash. They don’t need complex tax strategies or estate plaing. They just want their money to grow passively. For these folks, the cost savings are huge. You’re essentially getting a digital investment manager that’s incredibly efficient and affordable.

The Ceiling of Complexity

This is where the human advisor shines. If your financial life gets complicated – and trust me, it can – a robo-advisor might hit its limit. What if you’re self-employed with fluctuating income? What if you have significant assets, multiple investment accounts, or need sophisticated tax plaing to minimize your liabilities? Maybe you’re looking at selling a business or plaing for long-term care. These aren’t simple portfolio allocations. These require deep understanding, tailored advice, and often, a human who can coect the dots across your entire financial picture. That’s the ‘ceiling of complexity’ people talk about. Robots are great at the basics, but when things get truly intricate, you need a brain, not just an algorithm.

The Hybrid Approach: The Best of Both Worlds?

Increasingly, we’re seeing a middle ground emerge: the hybrid model. Think of it as robo-advisor efficiency combined with human oversight. Some firms offer automated investing platforms but also give you access to a human advisor for a higher fee. You get the low costs and convenience of the robo, but with the option to talk to a real person when you need them. This can be a fantastic compromise. You get automated portfolio management for your day-to-day investing, but you can still get personalized advice for those bigger, more complex questions. It’s like having a digital assistant for the routine tasks and a seasoned expert for the critical decisions. It’s a smart strategy for many.

Source : linkedin.com

What Does the Research Say?

Studies are starting to show that while robo-advisors can be effective for basic portfolio management, human advisors often lead to better long-term outcomes, especially when behavior coaching is involved. One study highlighted that investors using robo-advisors often lack the emotional support to stay invested during market volatility. CNBC noted that behavioral coaching from a human can be worth more than any investment return. Essentially, a good advisor keeps you from making costly emotional mistakes. It’s not just about picking wiers; it’s about preventing losers caused by fear or greed. This behavioral aspect is critical.

Trust and Satisfaction: A Human Factor

Building trust is huge in finance. Can you truly trust a black box algorithm with your future? Some research indicates that while users appreciate the efficiency and cost of robo-advisors, satisfaction often hinges on whether they feel understood and supported. A 2025 report on customer trust suggested that while robo-adviser technology is impressive, the human element remains a key differentiator for deeper client relationships. People want to know their advisor ‘gets’ them. They want empathy, especially when discussing sensitive financial matters. It’s more than just a transaction; it’s about peace of mind.

The Verdict: Who Wins?

Source : linkedin.com

So, are AI robo-advisors better than human brokers? It’s not a competition where one clearly knocks the other out. It’s about finding the right fit for you. If you’re young, just starting, have simple needs, and are cost-conscious, a robo-advisor is probably your best bet. You’ll save a ton on fees and get a solid, automated investment plan. If your financial life is complex, you need personalized advice, or you want that human coection and behavioral coaching to weather market storms, a good human advisor (or a hybrid model) is likely the way to go. Don’t just chase the cheapest option; chase the option that best serves your goals and your peace of mind.

Ultimately, the best approach often involves understanding your own needs. Are you disciplined? Do you have complicated taxes? Do you just need someone to tell you to hold on during a crash? The lines are blurring, with many firms offering a spectrum of services. The key is to know yourself, your finances, and what you expect from your financial partner. A machine can manage money; a human can guide your life. Which do you need more right now? It’s a big decision.

Frequently Asked Questions

Can a robo-advisor handle complex financial plaing needs like estate plaing or tax optimization?

Generally, no. While some advanced robo-advisors are adding more features, they typically stick to investment management. Complex tasks like estate plaing or highly specialized tax optimization usually require the expertise of a human advisor. Think of robo-advisors as great for portfolio building, not for intricate financial life mapping.

What happens to my money if a robo-advisor company goes out of business?

Don’t panic. Your investments are held by a separate custodian, not the robo-advisor company itself. So, if the company fails, your assets are still safe and can be transferred to another institution. Robo-advisors are regulated, and your accounts are typically insured up to certain limits by SIPC. It’s designed to protect you. Your money is generally safe.

Are robo-advisors really cheaper than human advisors in the long run?

Yes, almost always. The fees are significantly lower, often a fraction of what a human advisor charges. Over decades, these fee differences add up astronomically. While a human advisor might offer more services, the sheer cost savings from robo-advisors are hard to beat for basic investment management. You keep more of your returns.

Can I trust an AI with my financial future?

Trust is earned. Robo-advisors are built on algorithms and data, making them objective and unemotional. They won’t panic sell during a market crash. However, they lack the empathy and personalized understanding a human provides. For objective, data-driven investing, they’re solid. For nuanced life situations, you might want that human touch. It’s about finding your comfort level.

What’s the difference between a robo-advisor and a financial plaer?

A robo-advisor primarily focuses on automated investment management based on your inputs. A financial plaer, who is often a human advisor, takes a broader view. They look at your entire financial picture – investments, insurance, retirement, estate plaing, budgeting, taxes – and create a comprehensive strategy. Think of the robo as a specialized tool and the plaer as a holistic financial architect.