High-Yield Savings Accounts vs. Crypto Staking: Where Should You Park Your Cash?

Look, we all want our money to make more money, right? It’s that simple. You’ve worked hard for your cash, and letting it just sit there is like watching a leaky faucet. You’re losing potential. But where do you put it? Traditional savings accounts are basically offering pocket change. So, what’s the real deal with these two buzzy options: high-yield savings accounts and crypto staking? Let’s break it down.

Source : ledger.com

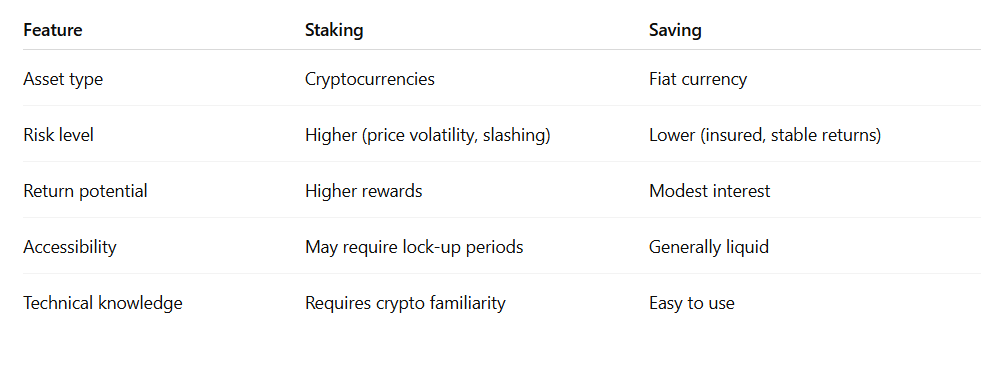

Forget those dusty bank brochures. We’re talking about putting your money to work. On one side, you’ve got the familiar territory of savings accounts, but with a juiced-up interest rate – the high-yield kind. Think of it as your dependable sedan. On the other, we have crypto staking, the shiny, high-performance sports car. It promises way bigger thrills, but also, you know, a few more risks. It’s a stark contrast, really.

The Savings Account Comeback (Sort Of)

Let’s start with the comfy option. High-yield savings accounts (HYSAs) are basically your standard savings account, but they offer significantly better interest rates than your typical brick-and-mortar bank. We’re not talking about the 0.01% you might get at a big national bank. HYSAs can offer rates that actually make a dent, sometimes anywhere from 4% to 5% APY (Aual Percentage Yield) or even higher, especially in a rising interest rate environment. It’s a solid play for your emergency fund or short-term savings goals. You know, the money you might need next month for a new fridge or that unexpected car repair. The key here is safety and accessibility.

These accounts are typically FDIC insured up to $250,000 per depositor, per insured bank, for each account ownership category. That’s a mouthful, but basically, your money is protected by the government. If the bank goes belly-up, you’re still good. Plus, you can usually access your funds whenever you need them, maybe with a few withdrawal limits per month, but it’s generally easy. No weird lock-in periods. This predictability is a huge draw for many people who’ve been burned before or are just risk-averse. It’s a low-stress way to earn a bit more.

Enter Crypto Staking: The High Roller Option

Source : reddit.com

Now, let’s talk about crypto staking. This is where things get interesting, and frankly, a lot more volatile. Staking is how you earn rewards on certain types of cryptocurrencies, specifically those that use a Proof-of-Stake (PoS) consensus mechanism. Instead of just holding your crypto, you ‘stake’ it – essentially locking it up for a period – to help validate transactions and secure the network. Think of it like being a shareholder who also helps run the company. In return for your service, you get rewarded with more cryptocurrency.

The potential returns here? They can be astronomical compared to HYSAs. We’re talking APYs that can range from 5% to a staggering 20%, or even 50%+, depending on the specific cryptocurrency, network conditions, and how long you lock up your assets. Some platforms even advertise higher rates, though you need to be incredibly wary of those. It’s a way to generate passive income in the crypto world, and it definitely beats traditional banking for sheer earning potential. You’re essentially betting on the success of the crypto project itself.

The Big Staking vs. Saving Showdown

So, what’s the real difference? It boils down to risk, reward, and accessibility. HYSAs are your safe bet. They’re insured, predictable, and you can get your money out easily. The returns are modest but steady. Crypto staking, on the other hand, is a wilder ride. The potential returns are much higher, but so are the risks. You’re not FDIC insured. Your staked crypto’s value can plummet, meaning even if you earn more coins, their dollar value might be worth less than when you started. It’s a gamble, plain and simple.

Consider this: you stake $10,000 worth of a crypto coin that pays 10% APY. Great, right? But if the value of that coin halves overnight due to market news, you’ve now got $5,000 worth of coins, even though you still have the same number of coins. Plus, your staked assets are often locked for a specific period. Can’t touch ‘em. This lack of liquidity is a major downside compared to the easy access of HYSAs. It’s about understanding what you’re willing to lose.

What About the Risks? Let’s Get Real.

Okay, let’s not sugarcoat the risks of staking. First off, market volatility is your biggest enemy. Cryptocurrencies are notoriously unpredictable. A tweet from Elon Musk or a new regulation can send prices spiraling. If you stake a coin and its price crashes, you could lose a significant chunk of your principal investment. This is the harsh reality that many new crypto investors learn the hard way. It’s not just about earning yield; it’s about the underlying asset’s value.

Then there are platform risks. You’re trusting a third party (an exchange or a staking pool) to hold and stake your assets. Hacks happen. Exchanges can go bankrupt (remember FTX?). If the platform you use gets compromised or folds, your staked funds could be gone forever. This is why doing your due diligence on the platform’s security and reputation is absolutely critical. You need to know who you’re dealing with. As a great resource puts it, staking involves significant risks, and you should only invest what you can afford to lose.

And let’s not forget technical risks and slashing. In some PoS networks, if you, or the pool you’re in, act maliciously or are offline when you’re supposed to be validating, you can be penalized. This penalty, called ‘slashing,’ means a portion of your staked crypto is taken away. Ouch. It’s a way to enforce good behavior, but it’s another potential pitfall. It’s complex stuff, far removed from the simplicity of a savings account. You’re directly involved in the network’s operations, whether you realize it or not.

Source : changelly.com

HYSAs: The Boring (But Safe) Boring Option

High-yield savings accounts? Their risks are minimal. The main ‘risk’ is inflation eroding your purchasing power if the interest rate is lower than the inflation rate. But your principal is safe. You know exactly how much you have, and it won’t disappear overnight because of a crypto market crash. It’s predictable. It’s boring. And for a lot of people, especially those saving for a house down payment or retirement, that boring predictability is exactly what they need. It’s the financial equivalent of a comfortable pair of slippers.

Who Should Choose What?

So, who wins this showdown? It’s not a one-size-fits-all answer. It depends entirely on your personal financial situation and your tolerance for risk.

Choose a High-Yield Savings Account if:

- You need easy access to your money (emergency fund, short-term goals).

- You have a low risk tolerance and can’t stomach potential losses.

- You prioritize security and FDIC insurance above all else.

- You’re new to investing and want a simple, straightforward way to earn more interest.

- You want to park money that’s earmarked for near-term expenses (like a vacation next year).

Choose Crypto Staking if:

- You have a high risk tolerance and are comfortable with significant volatility.

- You understand and accept the risks of losing your principal investment.

- You’re investing money you don’t need access to for an extended period (long-term horizon).

- You’re already invested in cryptocurrencies and want to generate additional yield on your holdings.

- You’ve done your homework on specific cryptocurrencies and their staking mechanisms. Staking requires research.

The Hybrid Approach: Best of Both Worlds?

Honestly, most people don’t have to choose just one. You can absolutely use both! A lot of folks are using HYSAs for their foundational savings – their emergency fund, money for upcoming bills, that down payment fund. Then, they might allocate a small, speculative portion of their portfolio to crypto staking. This is for the ‘play money,’ the funds they’re willing to lose entirely in pursuit of higher returns. It’s a balanced approach that gives you the security of savings while still allowing you to dip your toes into the potentially lucrative (and risky) crypto waters. This strategy leverages the strengths of both.

Think of it like this: your HYSA is your safety net. Your crypto stake is your moonshot. You wouldn’t bet your rent money on a long shot, would you? But maybe you’d put $20 on it. It’s about building a diversified financial strategy that aligns with your life. Don’t put all your eggs in one basket, especially when one basket is insured and the other is made of digital lightning.

FAQs: Your Burning Questions Answered

Source : medium.com

Is staking crypto better than a high-yield savings account?

Better is a strong word. It really depends on what you mean by ‘better.’ If ‘better’ means potentially much higher returns, then yes, crypto staking can be better. But if ‘better’ means safer, more predictable, and insured, then absolutely not – a high-yield savings account wins hands down. Staking comes with significant risks like market volatility and platform hacks that HYSAs just don’t have. It’s a trade-off between risk and reward. As one expert puts it, staking is fundamentally different from traditional savings. Crypto savings differ from staking in crucial ways.

Is there a downside to crypto staking?

Oh yeah, there are downsides. The biggest ones are market volatility (the value of your staked crypto can crash), platform risk (the exchange could get hacked or go bankrupt), and liquidity risk (your crypto might be locked up and inaccessible for a period). Plus, there’s the risk of ‘slashing’ if the network penalizes validators. It’s definitely not a risk-free venture. You could lose your entire investment.

Is staking cryptocurrency a good idea?

For some people, yes. If you have a high tolerance for risk, understand the technology, have a long-term investment horizon, and are investing funds you can afford to lose, then staking can be a way to earn significant passive income. It’s a way to put your crypto assets to work. But if you’re risk-averse, need easy access to your funds, or are looking for guaranteed returns, then staking is probably not a good idea for you. Stick with HYSAs or other traditional investments.

What are the main risks of crypto staking compared to traditional savings?

The main risks of crypto staking are market volatility, where the value of your staked assets can drop significantly; platform risk, meaning the exchange or wallet provider could be hacked or go out of business; and liquidity risk, as your funds are often locked up. Traditional savings accounts, on the other hand, are typically FDIC insured, offer easy access to funds, and your principal is protected against market fluctuations. The risks are vastly different.

Can I lose money even if the crypto staking rewards are high?

Absolutely, yes. This is critical to understand. Even if a crypto offers a 20% APY, if the price of the underlying cryptocurrency drops by 50%, you’ve lost money overall. The high rewards are meant to compensate you for the extreme risk of price depreciation. You could end up with more coins, but those coins could be worth far less in dollar terms than what you initially invested. Never chase yield without considering the underlying asset’s stability.

Frequently Asked Questions

-

Is staking crypto better than a high-yield savings account?

Better is a strong word. It really depends on what you mean by ‘better.’ If ‘better’ means potentially much higher returns, then yes, crypto staking can be better. But if ‘better’ means safer, more predictable, and insured, then absolutely not – a high-yield savings account wins hands down. Staking comes with significant risks like market volatility and platform hacks that HYSAs just don’t have. It’s a trade-off between risk and reward. As one expert puts it, staking is fundamentally different from traditional savings. Crypto savings differ from staking in crucial ways.

-

Is there a downside to crypto staking?

Oh yeah, there are downsides. The biggest ones are market volatility (the value of your staked crypto can crash), platform risk (the exchange could get hacked or go bankrupt), and liquidity risk (your crypto might be locked up and inaccessible for a period). Plus, there’s the risk of ‘slashing’ if the network penalizes validators. It’s definitely not a risk-free venture. You could lose your entire investment.

-

Is staking cryptocurrency a good idea?

For some people, yes. If you have a high tolerance for risk, understand the technology, have a long-term investment horizon, and are investing funds you can afford to lose, then staking can be a way to earn significant passive income. It’s a way to put your crypto assets to work. But if you’re risk-averse, need easy access to your funds, or are looking for guaranteed returns, then staking is probably not a good idea for you. Stick with HYSAs or other traditional investments.

-

What are the main risks of crypto staking compared to traditional savings?

The main risks of crypto staking are market volatility, where the value of your staked assets can drop significantly; platform risk, meaning the exchange or wallet provider could be hacked or go out of business; and liquidity risk, as your funds are often locked up. Traditional savings accounts, on the other hand, are typically FDIC insured, offer easy access to funds, and your principal is protected against market fluctuations. The risks are vastly different.

-

Can I lose money even if the crypto staking rewards are high?

Absolutely, yes. This is critical to understand. Even if a crypto offers a 20% APY, if the price of the underlying cryptocurrency drops by 50%, you’ve lost money overall. The high rewards are meant to compensate you for the extreme risk of price depreciation. You could end up with more coins, but those coins could be worth far less in dollar terms than what you initially invested. Never chase yield without considering the underlying asset’s stability.